EMX Royalty: Creating Shareholder Value Through Royalty Generation

EMX Royalty (EMX: NYSE, EMX: TSX-V, 6E9: Frankfurt), a Vancouver-based company that specializes in precious, base, and battery metals royalties.

Investors looking to get into the mining sector have traditionally had two options to choose from. They could invest in ‘majors’ – well-established mining companies that operate large-scale mines and produce consistently year after year; or in ‘juniors’, usually smaller and newer companies that engage in financially risky exploration looking for new mineable mineral deposits that can later be put into production.

While there are significant upsides to investing in both majors and juniors, each choice carries with it significant inherent risks that a savvy investor must be wary of – everything from fluctuating commodity prices, potential political risks depending on the location of the project, geologic and metallurgical risks, environmental risks, even social risks associated with the mining industry.

So what is a potential investor to do to mitigate these risks? One option would be to sidestep the majors and juniors altogether and opt for a third choice – a mineral royalty company. Mineral royalty companies avoid many of the risks associated with traditional mining companies, while reaping many of the benefits.

One of the leaders in the mineral royalty space is EMX Royalty (EMX: NYSE, EMX: TSX.V, 6E9: Frankfurt), a Vancouver-based company that specializes in precious, base, and battery metals royalties, with a stake in over 250 diverse mineral properties scattered across the globe.

According to Scott Close, EMX’s Director of Investor Relations, the value proposition for a mining royalty company like EMX is fairly straightforward, “Typically over the life of a mine, the resource expands by 100% from when it was initially brought into production. None of that cost is borne by the royalty holder. That is borne solely by the mine operator. And we're the benefactors of that.”

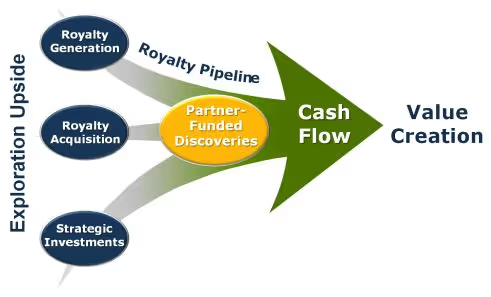

EMX Royalty’s primary means of assembling their royalty portfolio is through a strategy of royalty generation. The company employs a large team of geologists to scour the globe for prospective mineral real estate. When they find a viable site, they either stake the property, or pick it up in a government auction. According to Close the process is highly specialized, and the company does their homework before investing in a new property, “We do a lot of geologic due diligence to find prospective open ground, we secure that ground, then we go in and perform basic inexpensive surface or near-surface exploration and strive to find enough signs of mineralization or outright mineralization to entice another company to come in and buy the project.”

The company generates cash from many different angles. For example, when the company sells off a property, they receive cash and or shares and they hold back a royalty on it. The buyers also make milestone payments to EMX – say if they come to a pre-feasibility study, or initiate production on the property; and if EMX stays on to manage the exploration of a property, they garner a 10% management fee.

The second plank of EMX’s business strategy is royalty acquisition. The Company looks to purchase existing royalties, commonly from third parties, when they can find them at reasonable pricing valuations.

EMX made two significant royalty acquisitions in 2021. One was the SSR Mining Royalty Portfolio of 16 global properties, including Gediktepe, a significant gold oxide and polymetallic sulfide project in Turkey, currently in production. That mine will see EMX generate revenue in multiple ways, including a 10% net smelter royalty on the gold oxide layer, and another 2% net smelter royalty on the underlying sulfide ore body.

The company’s other major acquisition last year was the Caserones copper molybdenum mine in Chile, where EMX has a 2.5% royalty that pays out quarterly. This royalty paid out around US$900,000 in the last quarter of 2021, and expects to top out at around $3.5 million for 2022.

“The Caserones acquisition is a game-changer,” says EMX Royalty CEO David Cole – a geologist and 30-year industry veteran serving a number of senior executive positions at Newmont, before joining EMX Royalty in 2003 (then known as Eurasian Minerals), “A lot of our future is tied to copper. The Caserones mine is a porphyry copper-molybdenum system in Chile. It’s one of the most prolific copper mineralized regions in the world. We’re delighted to have exposure to that.” Cole believes the life of the mine at Caserones to be around 30 years. “It’s akin to having a bond that pays in pounds of copper for decades into the future.”

The third plank of EMX’s business model is strategic investment – something that Scott Close feels is unique to EMX, “If we find a project within a company that we think is underrecognized in the market, but stands a significant chance of producing an outsized return, we may invest in that company directly and then lend them our geologic expertise to help them advance that and hopefully realize a significant financial gain.” EMX deployed this strategy at the Malmyzh copper-gold property which they got involved with in 2011. They used their geologic intellect and business acumen to help advance the property, and in 2018 helped facilitate its sale, which deposited US$69 million into the company treasury.

EMX’s business strategy clearly has many opportunities to generate cash flow. The mineral royalty sector is becoming more competitive, with other entrepreneurial companies seeing the value of the royalty model. EMX’s closest match is Altius Royalty Corporation (ALS: TSX), though they have different mix of commodities than EMX. Wheaton Precious Metals (WPM: NYSE, WPM: TSX) is another company with a similar business model to EMX, but they are a streaming company and don’t deal in royalties.

EMX’s near-term goal is to become cash-flow positive, which Scott Close feels is just around the corner, “Our goal this year is to become decidedly and sustainably cash flow positive, which we are certainly on track to do; this will be a transformative event for the company. When we become cash flow positive and that drops to the bottom line and starts registering in the quarterly reports, you're going to see a material change in the share price.”

The company also hopes to pay a small dividend to investors this year, an unusual occurrence for a royalty company, but one that opens the door to institutional purchases from pension funds and other similar investment vehicles.

And of course, the company will continue to acquire more properties, which is the bread and butter of the operation, according to Close, “We've got in excess of 250 properties right now. There are 130 plus exploration properties that are available for purchase or partnership, plus over 120 royalty properties. So we just keep growing the portfolio. We are a global endeavor.”

And if all goes according to plan, EMX Royalties will become a cash-flowing endeavor for their shareholders as well.

For more information on EMX Royalty Corporation (TSX.V: EMX) please click the request investor info button.

FULL DISCLOSURE: EMX Royalty Corporation is a client of BTV-Business Television. This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional. Any action taken as a result of reading information here is the reader’s sole responsibility.

Latest Posts

Hot Companies

You might also like

Clinch Resources Expands Beyond Traditional Met Coal Into Specialty Carbon Markets

Clinch Resources is leveraging its metallurgical coal assets to enter the higher-margin specialty carbon market, supplying high-purity coal used in steelmaking, semiconductors, solar panels, and water filtration. Backed by strategic investments, vertically integrated operations, and premium-quality assets, the company aims to capitalize on growing demand for domestically produced specialty carbon.